LEVEL II

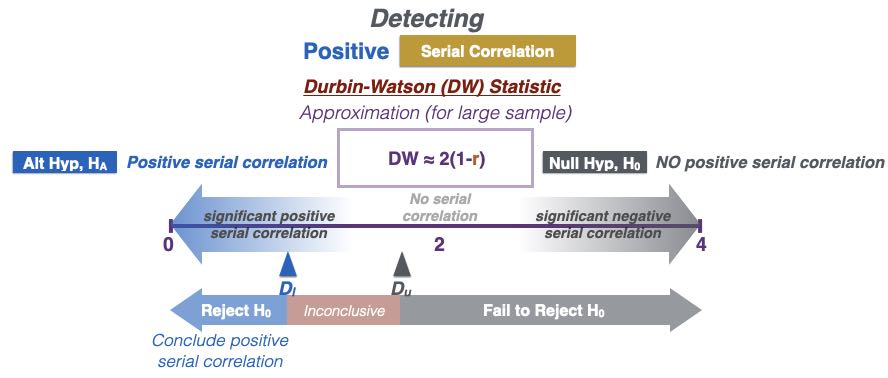

The Durbin-Watson (DW) test is a statistical test used to detect autocorrelation in the residuals of a linear regression model. The test statistic is a value between 0 and 4, with the null hypothesis being that there is no autocorrelation in the residuals. A value close to 2 indicates no autocorrelation, a value less than 2 indicates positive autocorrelation and a value greater than 2 indicates negative autocorrelation.

The test statistic is calculated using the residuals of the regression model, and it compares the differences between consecutive residuals to their average. An approximation for a large sample is as such:

DW ≈ 2(1-r)

r: correlation coefficient between residuals from one period and those from the previous period

If the consecutive residuals are positively correlated, the differences between them will be small, resulting in a test statistic less than 2. If the consecutive residuals are negatively correlated, the differences between them will be large, resulting in a test statistic greater than 2.

One limitation of the Durban-Watson test is that it only applies to testing for first-order serial correlation, that is it only tests for the condition with a single time lag. The Breusch-Godfrey test is regarded as a more robust test as it can be designed to detect serial correlation for multiple time lags.